Macro View

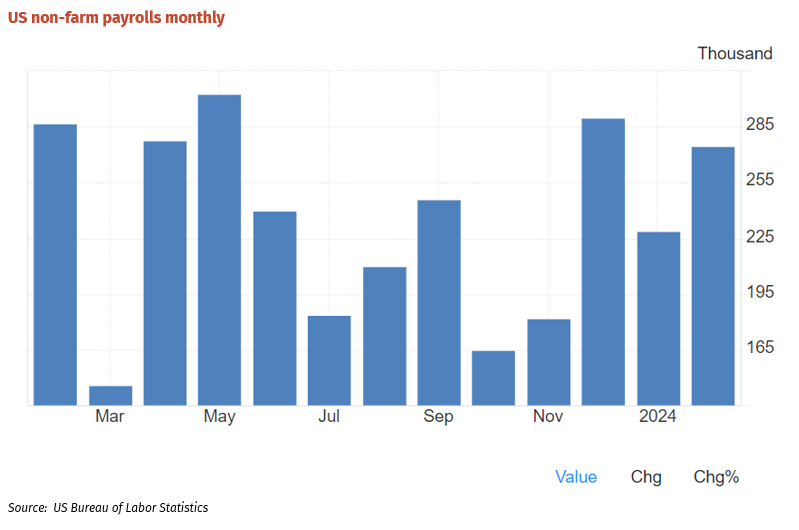

Wall St and more importantly the global bond markets place a high degree of degree of confidence in the US non-farm payrolls as a predictive economic indicator. It is, however, interpreted very differently by sections of the market with inherent conflicts of interest.

The strong February non-farm payrolls showed an employment surge in February of 275,000 new jobs but also large revisions of 167,000 fewer jobs recorded across the December and January periods. Sections of the market (blinkers on) screamed that the economy was not as strong as previously thought so the Federal Reserve would begin cutting rates next. Another section of the market revised its rate cut expectations out to a beginning in June and then followed by another 3 cuts in the second half. A small section of the market concluded that the average increase in employment over the entire December–February period was still well above market expectations and consistent with the US economy remaining robust. This group doesn’t see much chance of the US Federal Reserve being able to justify a rate cut this year for economic reasons.

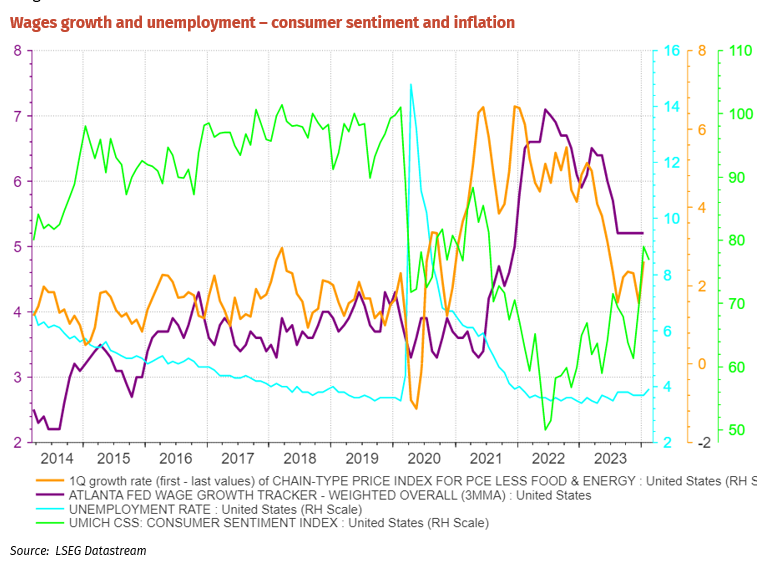

The payrolls data is very much a lagging indicator of actual economic activity. The employment data historically has reflected business decisions made 6-9 months earlier. Given the number of interest rate increases over the past 18 months the ongoing strength in the employment data is astounding. It is important to also note two other related economic indicators in the following chart. Firstly, after a steep fall post the pandemic lockdowns consumer confidence is rising again, and this is perhaps supported by wages growth remaining well above pre-pandemic levels. In time the inflationary impact on the household spending basket will be restored by this level of wages growth.

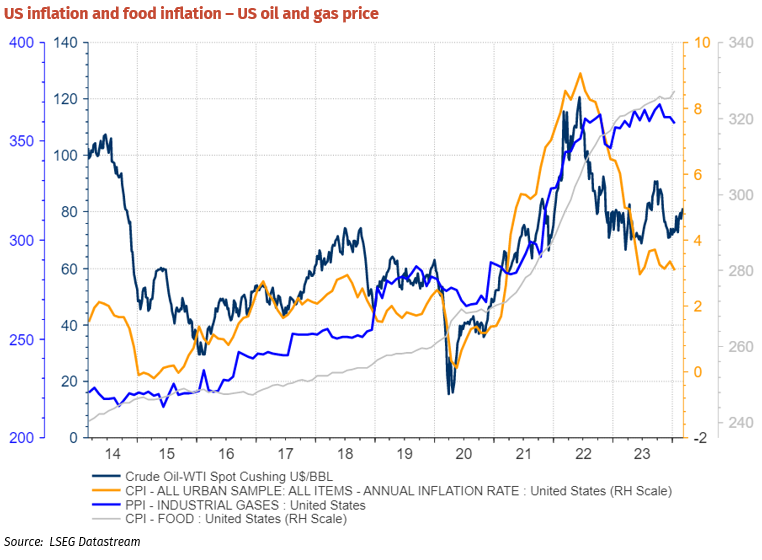

We have, for 6 months now, forecast that US inflation would begin creeping higher in the March quarter of 2024 because:

- A strong underlying economy led by services activity that has resulted in a strong labour market.

- Core inflation remaining well above target with a rising risk of feeding into wages growth.

- Energy costs rising.

If we were allowed to only use one chart to forecast inflation in the US, then we would use the following one that shows the impact of energy costs on food prices and headline CPI rates.

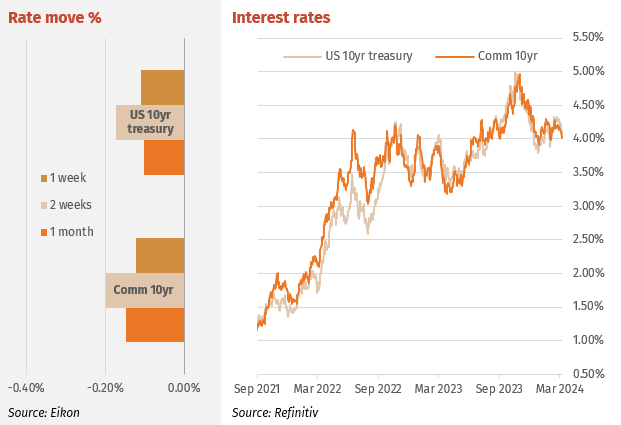

Interest Rates

Interest rates fell again over the week with markets overall thinking most economic data points to a Fed rate cut in June. However, as discussed below (page 4) it’s never that simple. 10-year treasuries fell by 0.11% over the week to 4.075%, getting closer to the recent December lows of 3.85%. Next week serves up a key piece of inflation data, the US core CPI.

Australian bond yield changes mirrored that in the US with the 10-year Comm. gov. bond falling by 0.12% to 4.01%, 2 years falling by 0.07% to 3.67%. A weak GDP number early in the week failed to move yields, indicating the market expected the real growth rate of just 0.20%. This is also what the RBA expected and hence is factored into its current rates view and commentary. The RBA expects annual GDP growth will go as low as 1.3% in June 2024 as it keeps rates high to slow the rate of inflation accelerating.

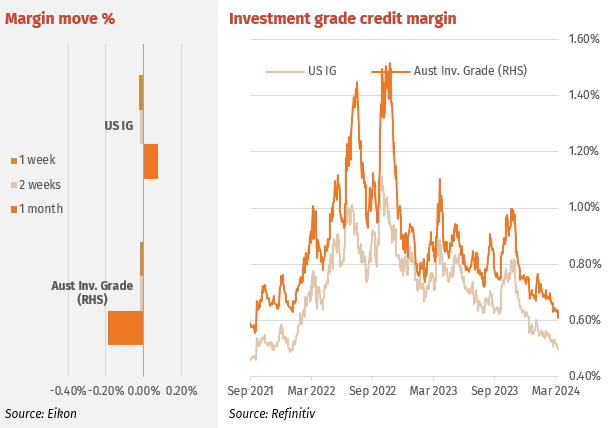

Major Credit Markets

Global investment grade (IG) were markets tighter over the week after the ECB held interest rates steady and Fed Chair Jerome Powell said that easing was likely in 2024, albeit with the requirement of inflation rates still falling. The US iTraxx index at 0.49% is at 2-year lows as is the European iTraxx at 0.65%.

The Australian iTraxx index also fell over the week to 2-year lows at 0.60% despite large IG issuance. The conclusion is that there are ample funds looking for a yield home. CBA issued US1.25bn of a Tier 2 note at treasuries+1.65% equating to 1.95% in AUD. Liberty Financial (rated BBB-) tapped its March 2028 FRN for $75m at BBSW + 3.45%. Stockland Trust (rated A-) issued $400m of a 10.5-year senior bond at 6.136%, a margin of 1.83%. Mizuho Bank (rated A) issued $750m of a 4-year senior FRN at BBSW +0.90%. Aurizon Network (rated BBB+) issued $350m of senior unsecured bonds at a yield of 6.1338%, a margin of 2.0%. Victorian Power Networks (rated A-) issued $450m of 5-year senior unsecured bonds at 5.057%, a margin of 1.18%.

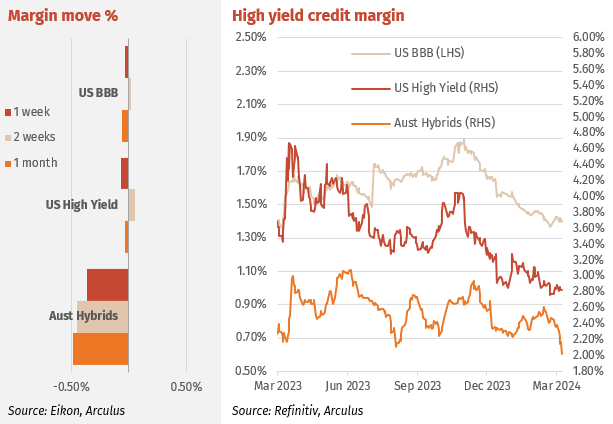

High Yield Markets

US high yield (HY) markets continue to perform with large issuance taking advantage of buying demand. HY credit spreads tightened by 7 points over the week. BBB spreads also continue to perform trading now at YTD lows, a margin fall of 0.16%.

Hybrids staged a huge rally in catch up to equity markets and after recent issues, clearing of the air on IPO stock. The 3 recent issues – ANZ, Bendigo and IAG – were all well bid and limited in supply of new stock. Pent-up buying has now spilled into the secondary market with demand across the margin curve. Additionally, many major banks’ ex-dividend pricing saw franking credits hold, which in turn results in a margin fall. The major bank average hybrid margin fell by a large 0.369% to finish the week at 2.02%, a level we have predicted for some time and last seen in January 2023. The average major bank long-dated hybrids margin fell 0.13% to 2.678%. The strong rally augers well for the listing of the three recent issues. In particular, the new ANZ will trade well. A margin fall of 0.13% to 2.77% will give a price of $100.77.

Listed Hybrid Market

Hybrids – recent hybrid IPOs, company’s other issues

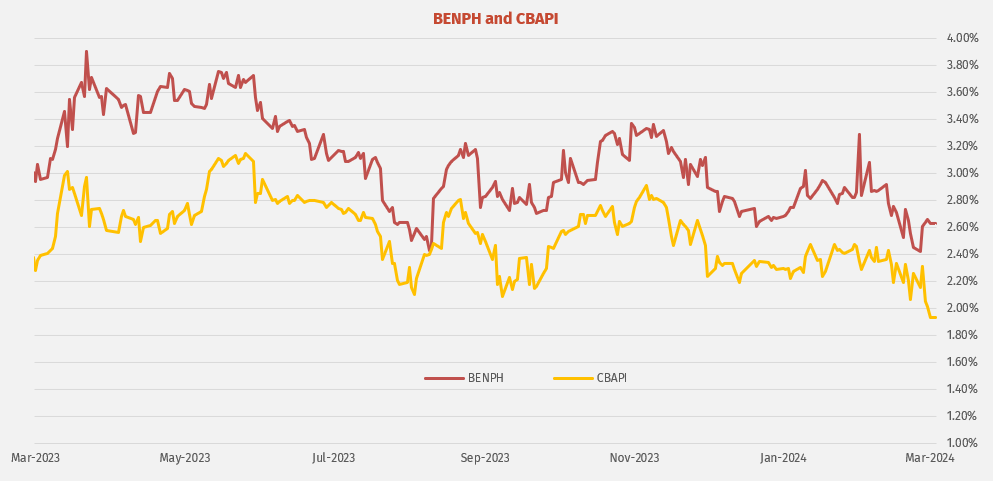

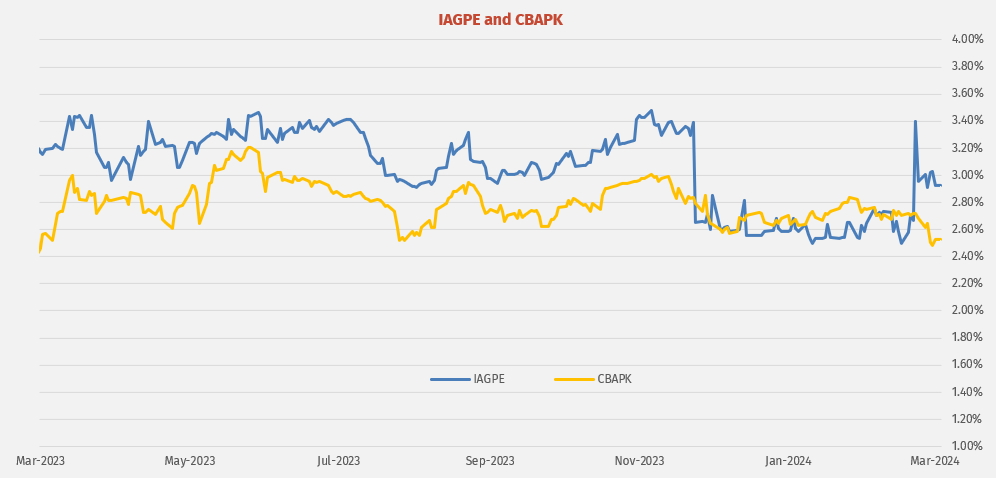

In past weeks both Bendigo Bank and IAG have issued new hybrids, Bendigo to partly replace the BENPGs and IAG a fresh new $350m issue. Below we look at the trading history for BENPH (June 2027 expected maturity) and IAGPE (June 2029 expected maturity) with similar maturity CBA hybrids as benchmarks. As noted above, the market has rallied in the past week to lows, each CBA hybrid flowing the broad market.

BENPH follows CBAPI’s margin movement quite closely, with an average premium in the past 2 years of about 0.60% (narrowing slightly over time, as maturity comes closer overall risk falls). Recently the premium has been 0.40%, which is more representative of how non-major bank hybrids trade to major banks. With the recent rally and some softening in the BENPH margin post the new BEN issue, BENPH could rally over the next week.

IAGPE. Typically, IAG hybrid margins have traded near major bank hybrids with similar expected maturities. The chart below shows the trading history for IAGPE and CBAPK, both expected maturity in June 2029. IAGPE has consistently traded at about a 0.30% premium to CBAPK, until December 2023 when IAGPE’s trading price did not adjust for ex-dividend and as a result the margin fell. More recently post the new issue announcement and the February dividend ex-date, the premium has been reinstated, forcing the market to correctly evaluate the IAGPE trading price.

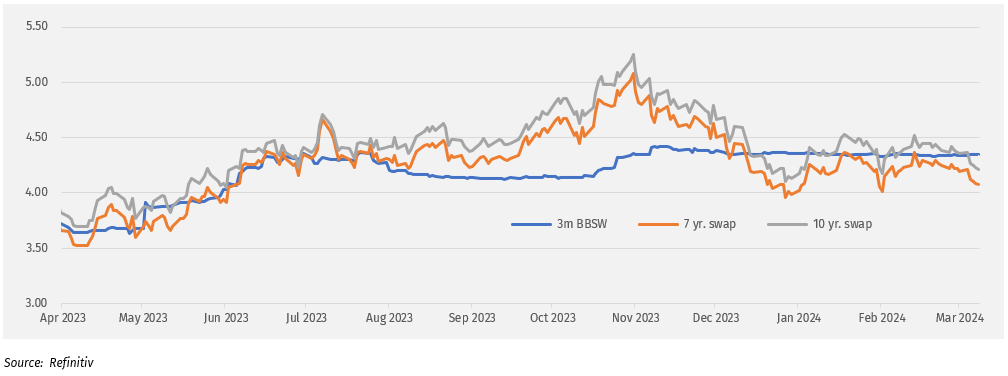

Australian rates

Swap rates drift lower following falls in long bond yields.

Swap rates:

- 10-year swap 4.23%

- 7-year swap 4.09%

- 5-year swap 3.99%

- 1-month BBSW 4.30%