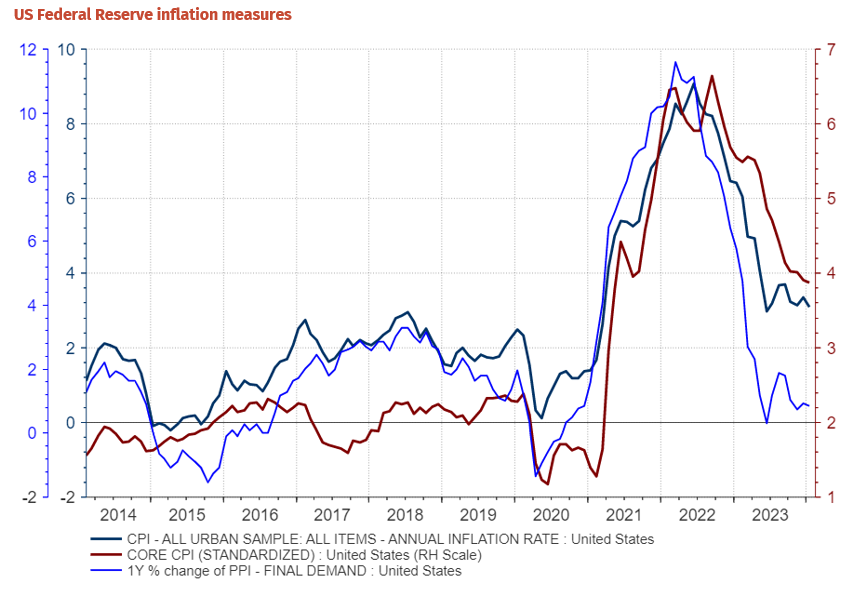

Last week began quietly enough so as not to wake market participants from their delirium in which “Goldilocks” is real and “immaculate” disinflation is possible. All of this fantasy stuff was shattered on Tuesday night when the US CPI results were stronger than expected. This was then compounded by the stronger than expected wholesale inflation readings (PPI) on Friday night. As the chart below displays prices are not actually rising… yet, but there is a growing realisation that inflation will at least track economic growth – Goldilocks is just a fairytale.

The move in the US yield curve was, perhaps, more significant that it looks on the charts because the move back to the highs of the week confirms that the trend has changed. The market may now trade the 5-year yield sideways for a period between the support at 4.10% to 4.40%.

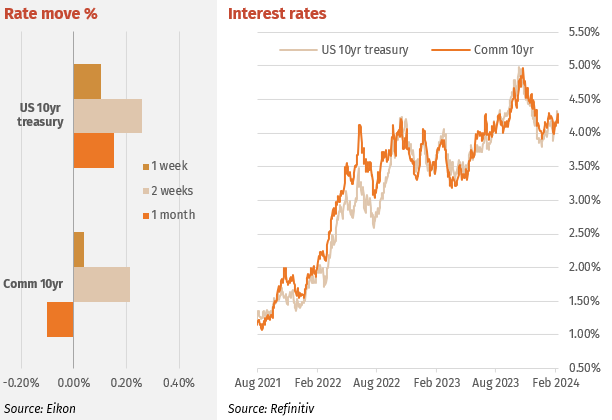

Interest Rates

After a slightly stronger than expected CPI, the PPI number also came in hot causing bond yields to rise again to 2024 highs. The December bond rally and rate cut narrative is slowly unwinding. Since 1st February, 1-year and 2-year yields are 31bps and 48bps higher respectively. At the weekend, the US 2-year hit 4.64%, a rise over the week of 0.16%, and 10-year treasuries to 4.28%, a rise of 0.10%. The US yield curve inverted slightly. In a similar fashion UK and German Bund rates are hitting 2024 highs, mainly driven by US bond rate rises.

Australian bond yields are also slowly tracking higher. Rates were higher across the curve especially 2 to 3-year bonds which are moving back to YTD highs. 10-year bonds are at 4.20%, well off the December year-end lows under 4%. A small rise in the unemployment rate gives little relief to the argument that inflation can be contained with the number of people in employment continuing to grow. The RBA governor tells the House Economics committee that the inflation fight is far from over. All this adds up to rates being on hold longer than the optimists hope.

Major Credit Markets

Major Credit Markets

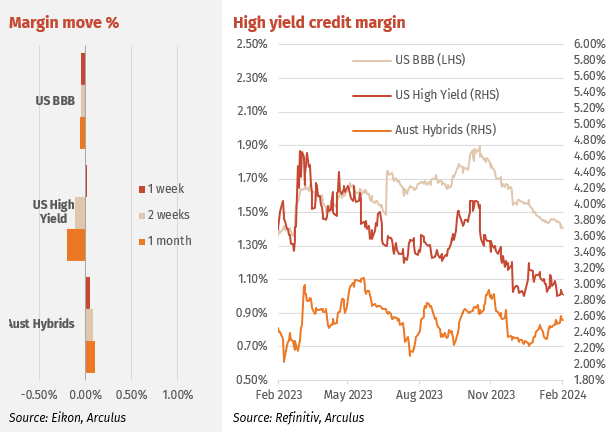

US credit spreads widened slightly albeit off recent lows and are being influenced day to day by the same thematic playing out on bond rates – the chance of rate cuts heavily influenced by inflation data. The stronger inflation prints are bad for credit margins as they decrease the likelihood of rate cuts and hence keep pressure on corporate funding rates.

Australian credit spreads remained strong similar to offshore markets. Bank senior major bonds were slightly stronger on light volume after DBS Bank Australia Branch (DBS Singapore rated AA-) issued AUD$1.25bn in 3-year fixed and floating rate senior unsecured notes at swap plus 0.77%. Bank Australia (rated BBB) issued AUD$300m of 4-year senior floating notes at BBSW + 1.70%. Major bank sub notes rallied especially at the long and short ends of the curve, the middle only showing small gains.

High Yield Markets

The US high yield (HY) sector remained strong given equity markets steadied and traded close to highs. Despite small outflows from HY funds, US HY issuance was over $7bn, above average and signaling investor appetite even at margin lows.

The flagged ANZ hybrid was finally launched, a $1bn+ issue with 7 years to first call and a margin range of 2.90-3.10%, coddled with a reinvestment offer for AN3PG. Demand was strong with books to be finalised mid this week with a possible size adjustment if ANZ gets the nod from regulators regarding the Suncorp bid.

Interestingly, overall hybrid margins moved wider on average by 5pts over the week despite longer-dated margins (the 4 issues > 6 years to maturity) falling by 8pts. Once the ANZ issue was formally announced the market was ignited with huge buying for longer-dated issues. WBCPM, the market’s longest-dated issue, was especially targeted rallying 13pts on 3 days of buy volume exceeding $20m.

Listed Hybrid Market

Hybrids – a crazy week on the curve

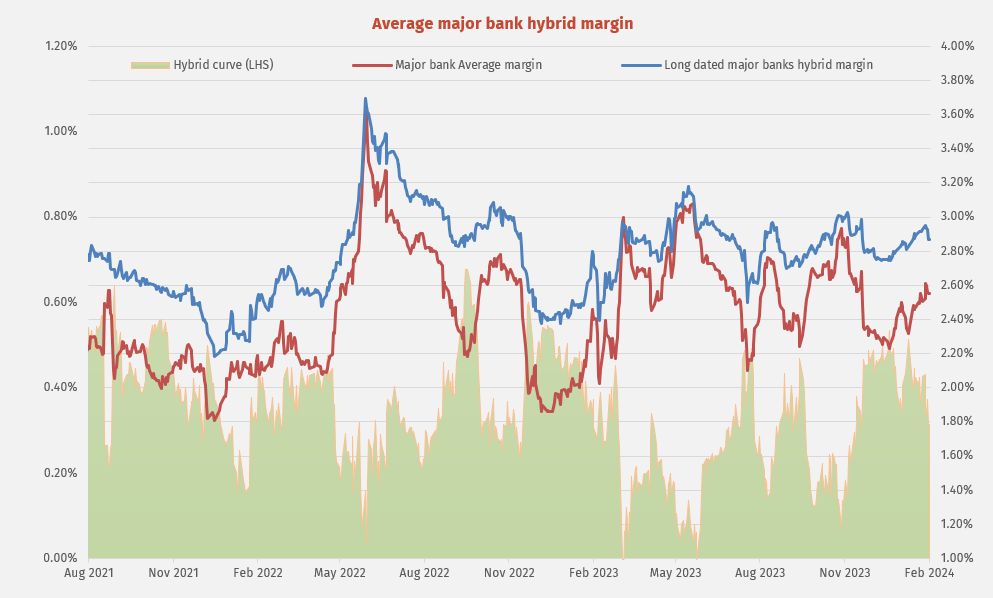

As mentioned above, after the ANZ issue was finally launched (14 Wednesday) and it became clear that new stock was going to be tight, market volumes jumped with over $50m of stock traded on the Wednesday as participants adjusted positions. By Friday the volume retreated to the recent daily average of $25m. Buyers came out in force for longer-dated issues with large buying at the long end of the curve especially in WBCPM which saw $20m of turnover in the 3 days. The chart below shows the curve changes: a rally for maturities after January 2029 however selling for the rest of the curve especially issue with 1 to 3-years until maturity. Hence, overall, the curve flattened as shown in the second chart.

The second chart shows the average hybrid margin for all issues and just long dated. The rally in long dated can be seen whereas the whole sector, represented by the red line, is still in uptrend.

Forward Interest Indicators

Australian rates

Swap rates are backing up along with the rise in bond yields.

Swap rates:

- 10-year swap 4.45%

- 7-year swap 4.29%

- 5-year swap 4.19%

- 1-month BBSW 4.30%