Investing is very difficult around key pivot points. If it were easy everyone would be getting double returns consistently. After a short lull in the economy over the past 6 months, we expect that some time in the March quarter we will begin to see inflation, or at least the factors that will lead to higher inflation, emerge. This pattern of a surge, then a lull only to see a surge again is something we have seen before in the 1970s Oil Shock. So far the US inflation rate appears to be following the same pattern. If the same pattern as that seen in the 1970/80s holds true, then the US CPI should reach a bottom in the March quarter then begin to rise.

Even if the Federal Reserve does get inflation back to 2.5% in the next 6 months it is likely that it will need to keep interest rates higher than they have been over the decade since the 2008 GFC. This is a concept that needs to be understood by investors. In the period from 2009 to 2020 investors were lulled into believing that the Federal Reserve would be able to get inflation under control with just a 200bps increase in rates and then it would cut rates at the first sign of asset price weakness. This was the Federal Reserve Put. The Federal Reserve Put is dead because inflation is going to prove to be more persistent due to the costs of the “green” transition and deglobalisation (onshoring of production from China due to supply chain risks). Even if we accepted that the “Goldilocks” fairytale that the market currently believes (inflation will magically decline without an economic contraction that increases unemployment significantly) is possible then we still expect that the ever-rising level of government debt will mean that US rates are going to have to remain elevated. What this means is that while the Federal Reserve keeps rates anchored at the short end we see the US yield curve steepening to reflect the increased price of financing increased debt.

Denial is not a river in Egypt. It might be convenient for short time periods, but eventually, will come acceptance that the US economy shows no real signs of an economic contraction, yet. Investors will remember that throughout most of 2022 many economists, market strategists and asset consultants forecasted that the US economy would be in a recession by the March quarter of 2023 (and the economic contraction would be more severe in Australia). They were wrong in 2022, wrong again in 2023 and at this stage we believe they will be wrong again in 2024. Last Friday night’s stronger than expected US non-farm payrolls data should have shocked the markets into a reality check. After nearly 2 years of rising interest rates from near zero to over 5%, the US economy remains fundamentally robust. The unemployment rate remains below full employment at 3.7%, the participation rate at 62.8% is near record highs, wages growth is still above 4% pa and now we are seeing a recovery in consumer confidence.

The following chart is very “busy”, as it contains a lot of data, but at key turning points forecasting is always difficult and complicated so all this data is necessary. Friday night’s strong employment data (dark green dashed line) was unexpected and not what the equity and bond bulls were hoping for. Wages growth in the US (purple line) remains too high and sticky (partly due to pandemic welfare remaining in place) for core PCE prices (the Federal Reserve’s preferred inflation measure) to fall any further. The natural lags in the economy are likely to deliver higher core inflation over the coming months as the strong wages growth, strong employment and strong fiscal spending keep aggregate demand too strong.

Interest Rates

The bond rally reversed on Friday after jobs data gave the market a reality check that the economy was in better shape than thought. Hence the rate cuts the market had been aggressively building may need recalibration. The 2-year US treasury rose back over 5%. 10-year treasuries increased by 5pts to 4.31%, a level still well below that of a week earlier. This week there is an array of data points and news, the US CPI and PPI, the US Fed rate decision and both the ECB and BoE meetings.

The BoJ lobbed its usual Christmas grenade into rate markets with comments that economic and wages strength will impact its next decision that may lead to a rate rise.

Australian rates followed US markets with falls across the curve of about 16pts. The 1-year rate is at 4.26% which gives some indication as to the market’s expectations of 2024 RBA action – a slight fall from current levels. Whether that includes another hike is unclear and really depends on the next quarterly CPI not due until mid-February.

Major Credit Markets

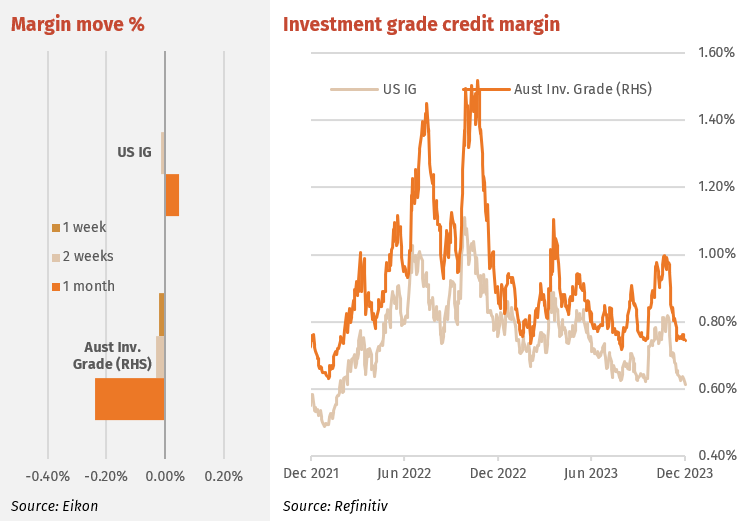

Investment grade (IG) bonds have maintained recent lows and are finding good or bad news a reason to remain steady: good economic news means better profits and bad news means more potential rate cuts. Either way buyers are currently content with strong equity markets in support.

Australian IG markets remained firm after the recent strength with buying volumes remaining strong but more skewed to floating rate securities given the recent rate rally. Bank senior bonds were steady but sub notes rallied across all maturities. Issuance was lighter but fell mostly to regional banks issuing

1-year notes. Hollard Insurance (rated S&P A) launched its first AUD security, $135m of a 15.25NC5.25 floating sub note (expected rating BBB) at a margin of 3.60%. Formed in South Africa in the 1980s, the Hollard Group now comprises insurance businesses throughout Africa, NZ and Australia. Hollard is the largest privately owned general insurance company in Australia underwriting brands such as Aust. Seniors and Woolworths.

High Yield Markets

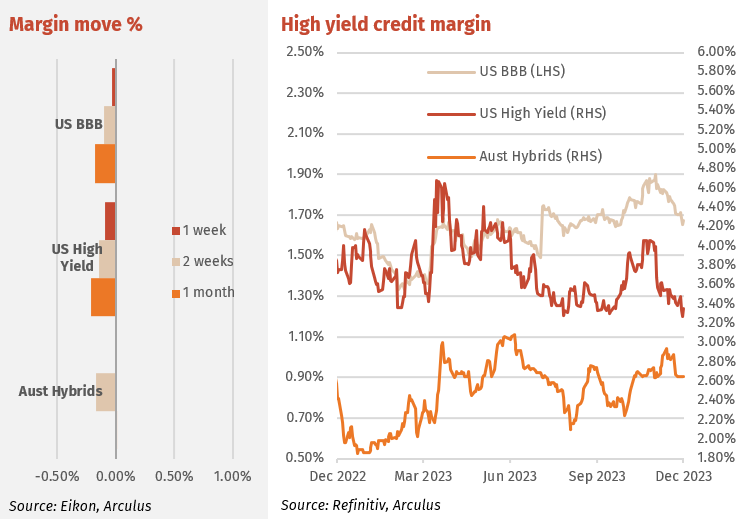

US high yield (HY) markets continue to rally with strong equity and steady credit markets. US HY corporate spreads have tightened by 1.02% YTD. The sector contains better rated companies than previous, with over 50% of HY rated BB. Poorly rated companies have leaked into the private credit sector. Money flow has increased into HY in recent weeks with over $2bn into the sector in the first week of December.

The hybrid rally increased speed with the average major bank hybrid spread falling by 0.24% for the week to finish at 2.30%, well below recent highs near 2.90% in mid-November. Many ANZ and CBA hybrids went ex-dividend to demand which saw much of the franking value not repriced causing falling margins. In particular, shorter-dated hybrids from these banks have fared best. The rally has not been confined to just the major banks, the non-majors have also been in demand, especially again short-term issues like BENPG and BOQPE. In contrast the Suncorp issues have underperformed, especially the longer-dated SUNPH and SUNPI.

Listed Hybrid Market

Hybrids mount catch up rally

Major bank share prices have been strong through November and the beginning of this month, posting a 2.16% return over the past week. Hybrid margins do follow the major moves in bank share prices and hence the recent share price rally has been one reason for the recent hybrid rally. Additionally, hybrid margins were yet to recover from the selling funding the recent Westpac hybrid IPO.

The chart below shows an index of the major banks’ total returns (see the green line and note that it is inverted to show the relationship with hybrid margins) and the average hybrid margin (red line). The fall in the green line in December 2023 illustrates the recent strong bank share price performance. Hybrid margins have some catch up to do and could easily rally to a 2% average given the relative levels prior, especially 12 months ago. Hence it is no wonder hybrid volumes are up and trading margins are contracting, especially for hybrids about to pay dividends. December is a large dividend month. Major bank hybrids going ex-dividend have only fallen the cash value and not the franking amount. Hence the franking value is obtained very cheaply when buying prior. Keep an eye on bank share prices. If the strength is maintained, hybrid buyers will remain aggressive into the New Year.

Forward Interest Indicators

Australian rates

Swap rates fall along with the general fall in bond yields. There is now little skew between short and long-term swap rates.

Swap rates:

- 10-year swap 4.60%

- 7-year swap 4.45%

- 5-year swap 4.33%

- 1-month BBSW 4.30%

Arculus Funds Management is an Australian asset manager of both public and private mandates.

They manage two retail public unit funds for DDH Graham:

- The Arculus Preferred Income Fund, formerly the DDH Preferred Income Fund

- The Arculus Fixed Income Fund, formerly the GCI Australian Capital Stable Fund

Platform Availability: BT Wrap / BT Panorama / Macquarie / Netwealth / Hub24 / Praemium / OneVue / Australian Money Markets / Ausmaq